2023 Contribution Limits and Why You Should Make a Contribution

A common question you hear in the retirement world is “how can I retire comfortably”, and we are constantly reminded how important it is to save for the future. IRAs (Individual Retirement Accounts) and Solo 401(k)s are some of the best tools created for those who choose to save money and create wealth for retirement through investing. Vehicles like this provide tax advantages for retirement savings, deferring taxes until distribution age or potentially making it to where an individual never has to pay taxes on growth at all!

Now that another year has almost come and gone, and the temperature isn’t the only thing changing as the year comes to a close. The IRS recently announced that contribution limits for various IRAs and retirement accounts will be increasing this year, and we have all the updates! Many investors have already started planning for 2023, and you can join them with these helpful updates.

Why Is It Important to Contribute to Your Self-Directed IRA Every Year?

With Self-Directed IRAs being one of the most powerful tools for future planning, it’s no surprise that there are countless reasons why it’s important to contribute to your retirement account, but we’ve listed the top three reasons here. First, when you contribute to a Self-Directed IRA, you receive tax benefits, like tax deductions and tax-free distributions! Accounts like Traditional IRAs provide the opportunity for tax deductions when you make contributions. Other accounts like the Roth IRA help the money you contributed grow tax-free.

By contributing, you are also putting your money to work and can watch it grow. Contributing to your Self-Directed IRA means you have more money to work with when you’re investing. The more deals you can do, the more money you can make. Lastly, you’ll be able to create more wealth for your future when you start to contribute early. The sooner you begin making yearly IRA contributions, the longer your money has to compound. Making a contribution every year helps it grow much faster.

With the announcement of the 2023 contribution limits, it’s important to note that you still have time to contribute for 2022. Every contribution counts, and as previously mentioned, each year that you miss out on making your yearly contribution is another year of missed compounding growth! Check out the 2022 contribution limits here or keep reading to find out what’s new for 2023 in the paragraphs below.

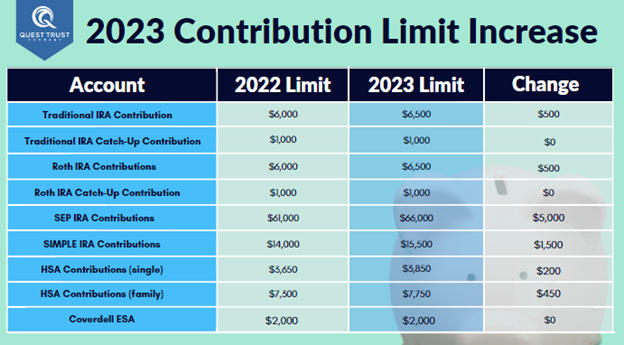

Traditional and Roth IRAs

The contribution limits for these two personal plans increased $500 from $6,000 in 2022 to $6,500 in 2023. Additionally, the age 50 catch-up limit remains, as it is always fixed by law at $1,000. The income ranges that determine one’s eligibility to make deductible contributions to Traditional IRAs or to contribute to a Roth IRA also increased, and you can read more about those numbers here.

Employer Plans

Employer plans, like SEP IRAs and SIMPLE IRAs, saw a change, as well. For SEP IRAs, contribution limits will increase to $66,000 per year for 2023, up $5,000 from 2022 which was $61,000. The amount one is allowed to contribute to a SIMPLE IRA increased to $15,500, up from $14,000. If you are age 50 or over, the catch-up contribution limit also increased, making it possible to contribute an additional $3,500 for 2023, up from $3,000 in 2022. For those with a Solo 401(k), the limit for the total contribution is increasing from $61,000 to $66,000 ($67,500 to $73,500 for those 50 and older). Solo 401(k) contributions work a bit differently than other accounts, so if you hold this type of account and still have questions about your allowed contribution, speak to a knowledgeable CPA or call a Quest Trust Solo 401(k) specialist!

Health Savings Accounts

The Health Savings Account, or HSA, contribution limits are expected to increase, too. For single coverage, it will go up to $3,850 for 2023, an increase from the $3,650 limit in 2022. For HSA accounts with family coverage, you can expect to see the limit go up from $7,300 in 2022 to $7,750 in 2023. These were already announced previously. Those who are 55 or older will still be able to contribute an additional $1,000.

Coverdell Education Savings Account

The Coverdell ESA will be one of the self-directed accounts that will remain the same. Just as in 2022, the maximum contribution limit for Coverdell accounts will be $2,000 per child per year in 2023.

For those who can take advantage of building their IRA during this time, understanding the different ways to contribute and the benefits of maximizing your account can make all the difference in your overall wealth building strategies. Getting ahead and familiarizing yourself with the 2023 contributions limits will help you prepare and budget for the new year, so as you start preparing for the end of the year be sure to keep contribution limits in mind. It’s never too early to start planning, and if you ever have questions about how to make a contribution to your Self-Directed IRA, a Quest Trust Company representative will be happy to help.